Keeping 'Em Honest: Wall Street's Track Record Is Not Good

Published Friday, January 19, 2018 at: 7:00 AM EST

Every December, Barron's, the weekly financial magazine, asks Wall Street strategists to pick the best and worst sectors to invest in, and every year their picks perform poorly relative to the unmanaged Standard & Poor's 500 index. 2017 was much the same.

The strategists include brilliant economists, but economists are not seers.

It's not uncommon for the consensus forecast of economists to fail to predict if the economy will expand or fall into a recession - a question with just two possible answers.

Picking the best and worst investment from among 10 possible industries is much more difficult.

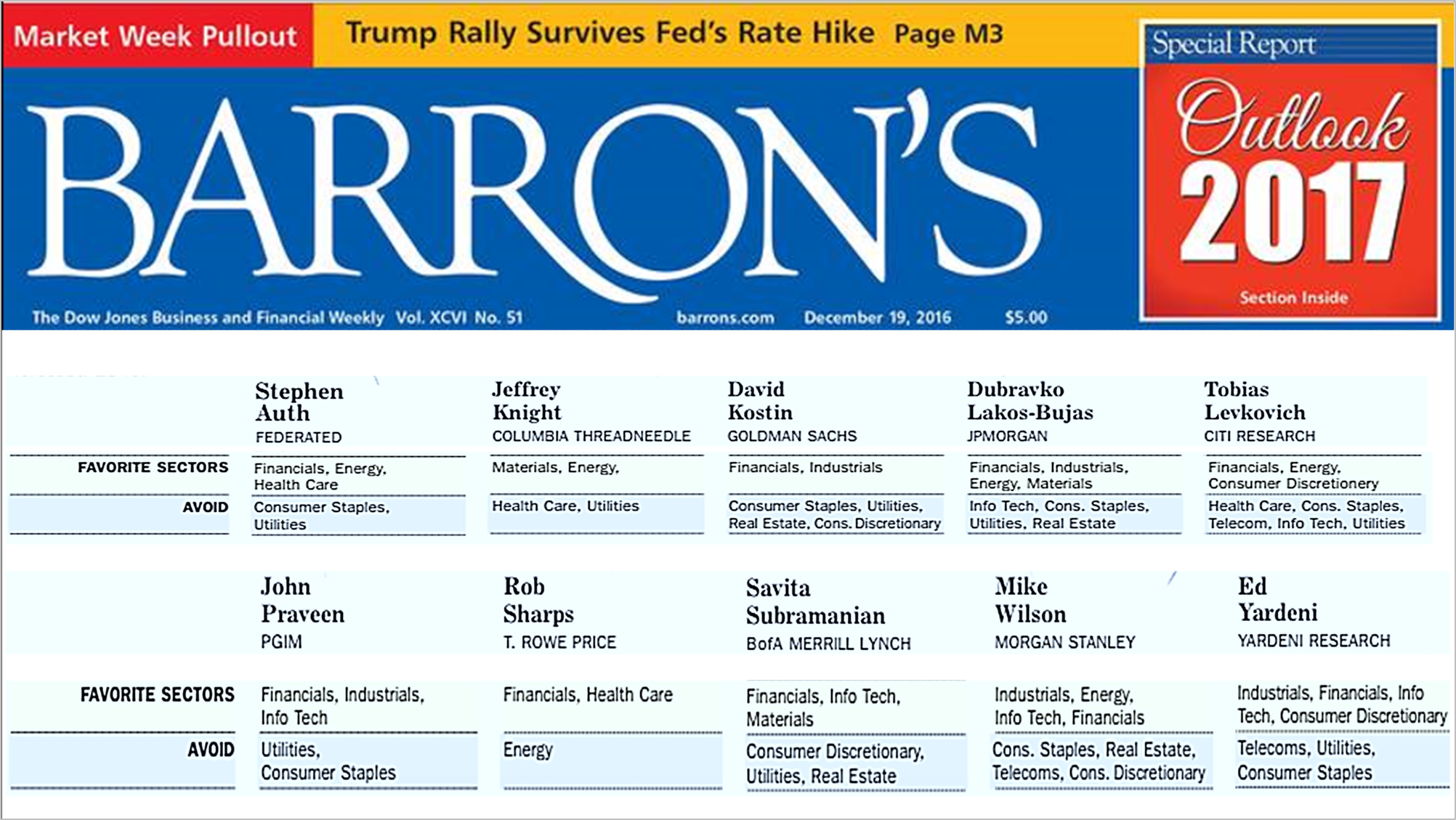

On December 19th, 2016, Barron's published its annual outlook for the year ahead, featuring forecasts from 10 "top" Wall Street investment strategists.

Every year, the respected financial weekly publishes its panel's stock market predictions, including the industry sectors they advise to buy and which they advise to avoid.

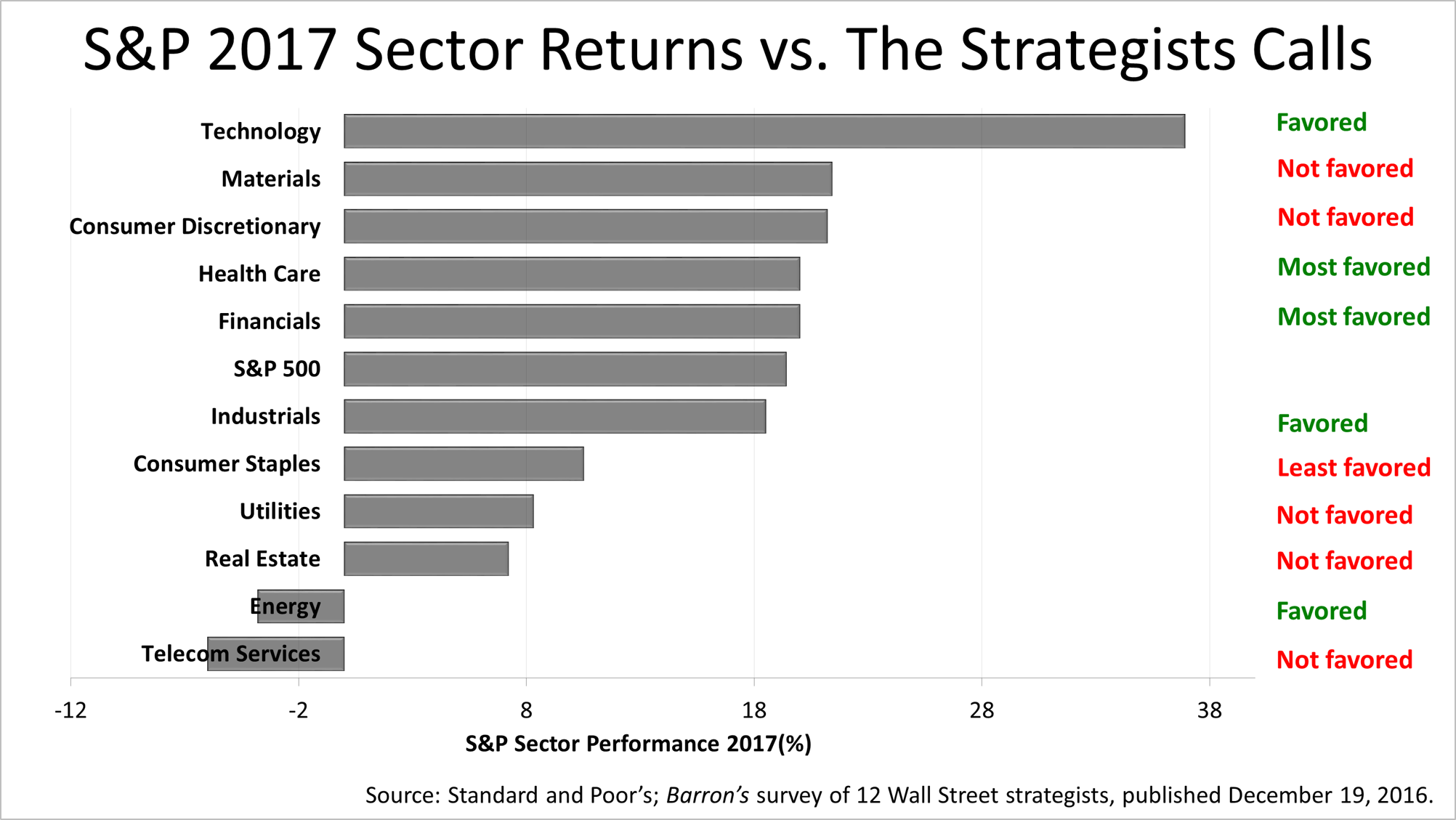

The 2017 sector picks and pans were published on December 19th, 2016. The 10 strategists, as a group, favored tech stocks and they got that right. That was a good call. But they missed the call on the second- and third-best performing sectors.

The sectors the 10 strategists were most bullish on in December 2017 were health care and financials, and they returned fractionally more than the S&P 500. For the two most-favored sectors to perform only about as good as the unmanaged index is not a great outcome.

The strategists did pan telecommunications and that was a good call; energy shares, as measured by the S&P 500 Energy sector index, lost about 5% in 2017. Meanwhile, the strategists favored energy stocks but that sector suffered about a 3% loss in value.

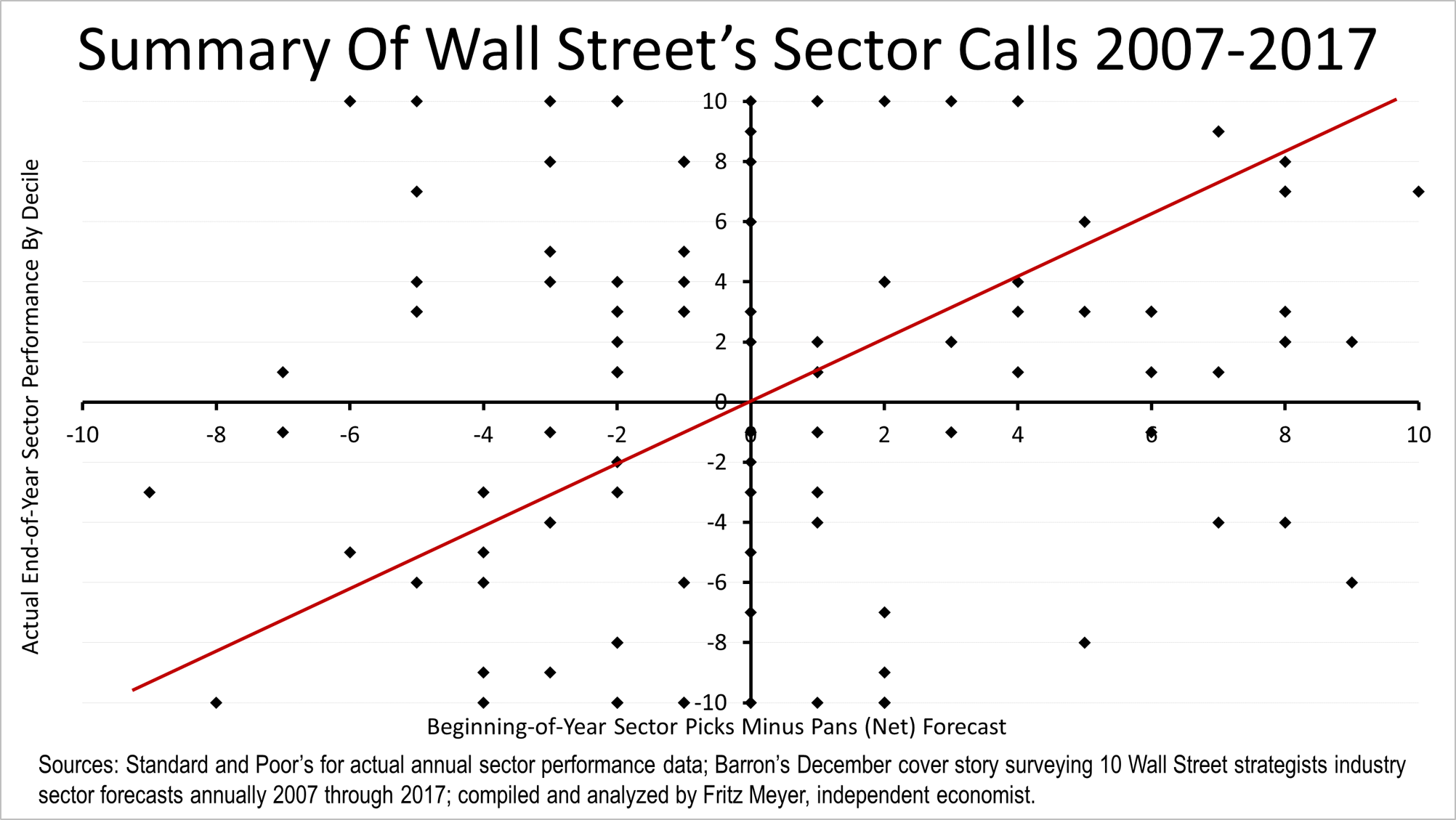

This picture shows just how off target Wall Street's strategists picks in Barron's have been since 2007.

The data on the Barron's strategists' forecasts has been tracked annually since 2005 by independent economist, Fritz Meyer, whose research we license.

If Wall Street's strategists' sector forecasts over the last 10 years had been correct, then the black dots would lie along the red line.

The random performance of Wall Street's advice is plain to see.

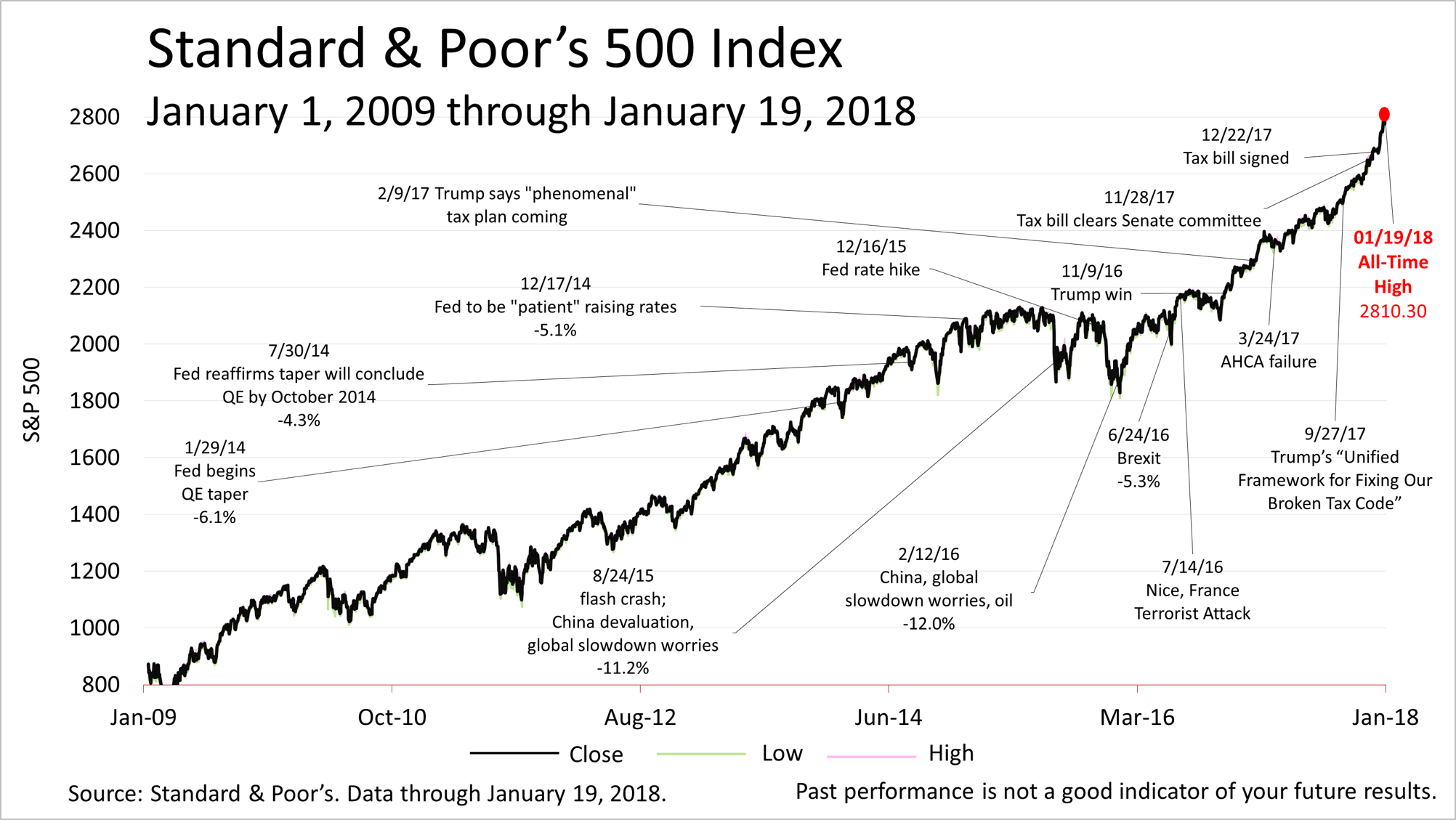

The Standard & Poor's 500 closed the week at 2810.30, another new record high price in an almost uninterrupted surge that began after the November 2016 election, and lately has gained strong momentum.

Yet plenty could go wrong anytime. A constitutional crisis, the nuclear standoff with North Korea and events that used to be unimaginable. Economists at the Fed could make an interest-rate policy mistake by quashing growth or allowing the economy to overheat and inflation to surge, or investors may suddenly turn their focus to the $19 trillion U.S debt and unsustainable fiscal path. A 10% or 15% drop could occur on a flash of bad news, and the chance of a bear market decline of 20% or more increases as the eight-and-a-half-year bull market grows older.

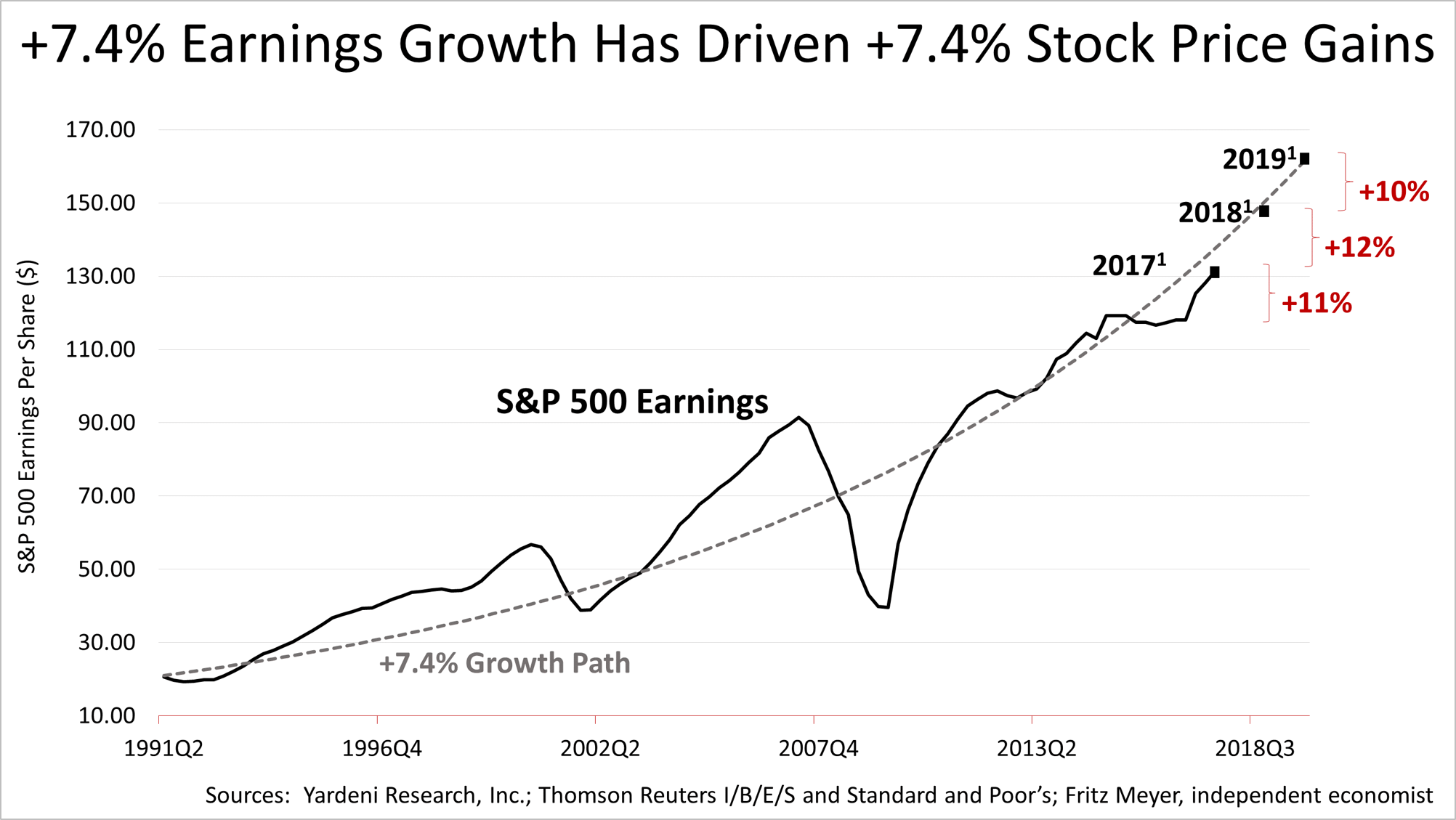

On the other hand, the economy now shows no sign of slowing. Smashing earnings growth is expected for 2017, 2018 and 2019.

Since April 1991, profits at America's 500 largest liquid companies have grown at an average annual rate of 7.4%, and a dollar invested in the average company over this 26-year period averaged a 7.4% total return annually. Projecting continued earnings growth of 7.4% would put prices on the trajectory indicated by the black dots. However, earnings growth is expected to be much higher than 7.4%. For 2017, 2018 and 2019, earnings growth of 11%, 12% and 10% is what's expected.

This explains why the S&P 500 price is spiking and why the financial press is filled with worry that stocks are in a bubble.

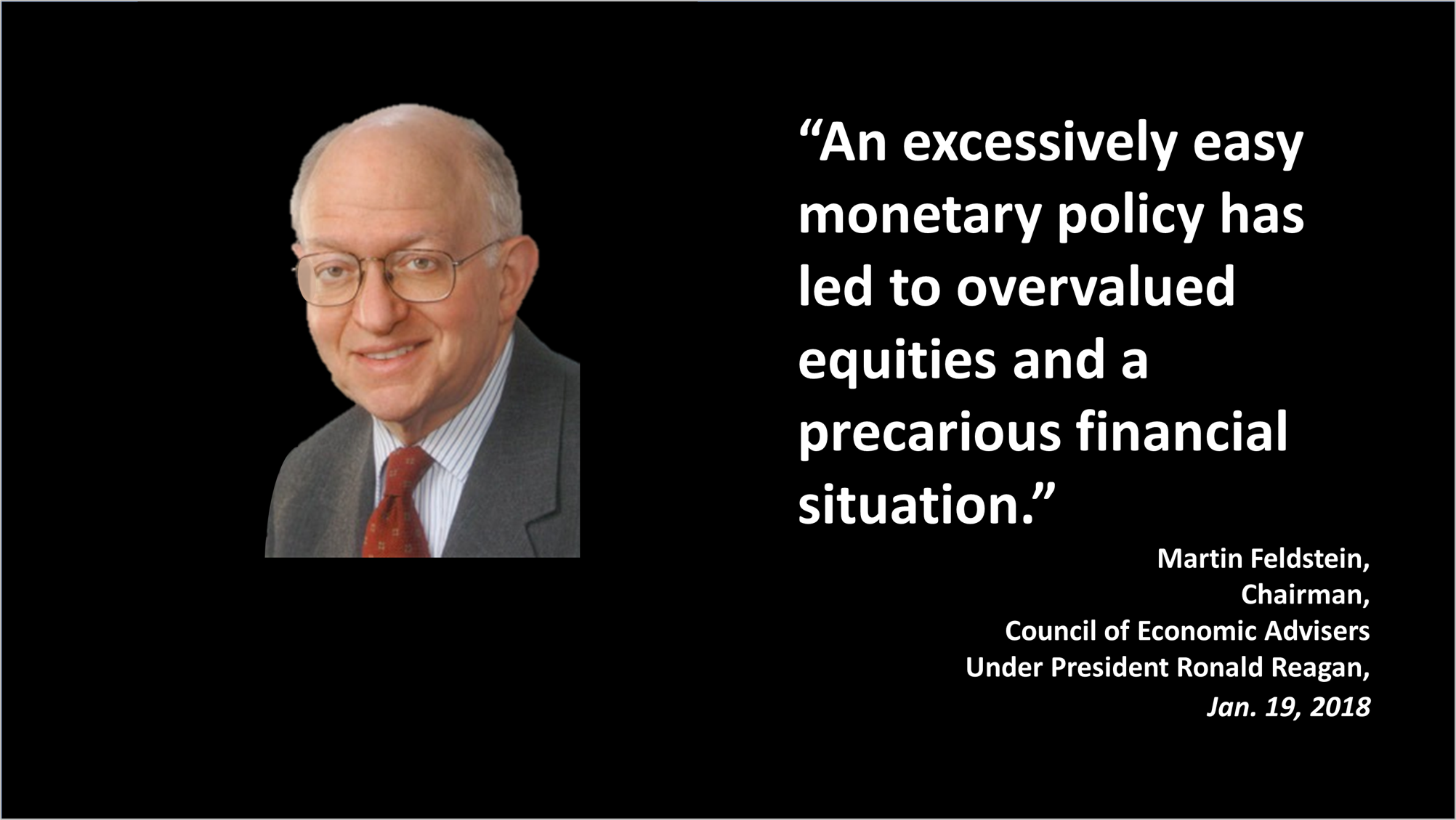

For example, Martin Feldstein, chairman of the Council of Economic Advisers under President Ronald Reagan, writing in today's Wall Street Journal, warned: "An excessively easy monetary policy has led to overvalued equities and a precarious financial situation."

It is reminiscent of former Federal Reserve Board chair Alan Greenspan's warning of "irrational exuberance" in stocks in December 1996. It took over three years for stocks to peak from that warning.

But what's different this time is that this stock price ascendance is not predicated on rising enthusiasm, but rather on rising earnings. So, this bull market could go on for longer.

12017 (estimated), 2018 (estimated) and 2019 (estimated) bottom-up S&P 500 operating earnings per share as of January 5, 2017: for 2017(e), $131.47; for 2018(e), $147.23; for 2019(e), $162.22. Sources: Yardeni Research, Inc. and Thomson Reuters I/B/E/S for actual and estimated operating earnings from 2015. Standard and Poor's for actual operating earnings data through 2014.

This article was written by a veteran financial journalist based on data compiled and analyzed by independent economist, Fritz Meyer. While these are sources we believe to be reliable, the information is not intended to be used as financial advice without consulting a professional about your personal situation.

Indices are unmanaged and not available for direct investment. Investments with higher return potential carry greater risk for loss. Past performance is not an indicator of your future results.

© 2024 Advisor Products Inc. All Rights Reserved.